Your (gov’t mandated) free credit report and how to do it.

Breakdown

Why should you consider running a credit report on yourself? Imagine someone rather unsavory in… I dunno, Louisiana, taking out a loan for a shiny new boat… in your name. Without your credit frozen, how would you even know? Credit reports reveal a wealth of useful information, from tracking your financial health to catching potential red flags like this. Additionally, at this point in our current technological cycle of “Everyone’s personal information has been leaked at some point and is purchasable online”, it’s a good idea to be proactive about checking on this stuff. In this week’s newsletter, we’re keeping it simple - walking you through how to pull your credit report and what surprises (good or bad 😬) you might uncover.

The ONLY site to use

If you google “Free credit report”, you’re gonna get hit with 30 different websites, 5 ads, and 12 Amazon book recommendations. The only website that is provided by the government through the Free Credit Reporting Act (FCRA) is https://annualcreditreport.com - that’s it! You can also get credit reports directly from the 3 bureaus (Equifax, Transunion, Experian), but those will require you to create accounts with them and they do their best to put it behind popups and full-screen ads promising that if you just spend some money with them they’ll give you that report and SO MUCH MORE! Oh, and not to mention the spam you’ll get signed up for as well. Incredibly annoying.

With that link above you get to cut out all of the crap the bureaus give you on their site and get straight to the point. Also, if it wasn’t obvious in the name, this is a yearly thing, however, you can space out your reports as much as you want from the individual bureau’s throughout the year. Meaning, say March you run it with Experian, August with Transunion, and December with Equifax - that’s completely fine.

Your free credit report is also considered a “soft pull” on your credit and is only visible to you, so running this has no affect on your credit score.

Let’s do it live

So I have not run my credit report this year and decided to go ahead and walk through the steps just in case they had any major changes before writing this, so let’s get through it.

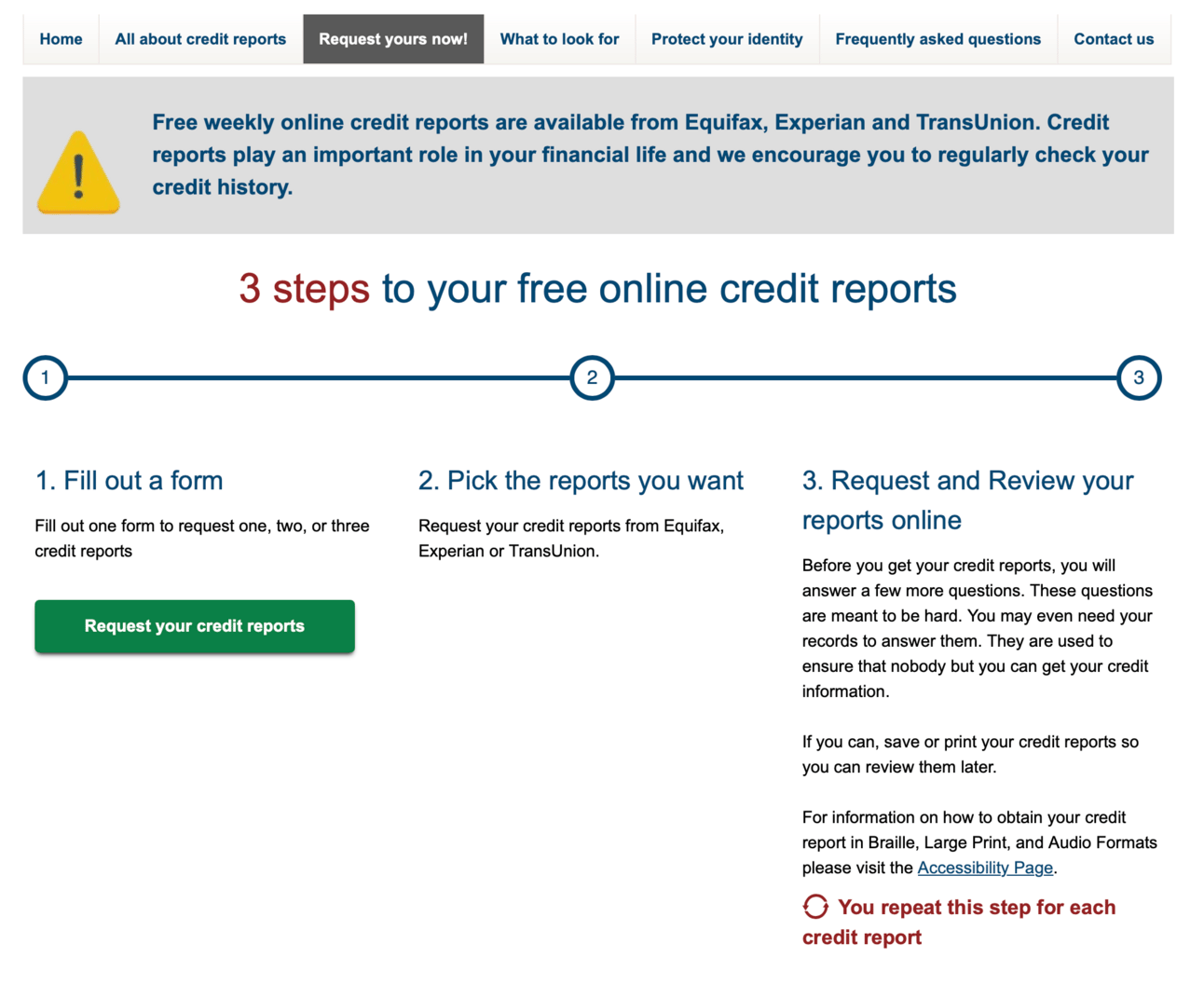

First you’re going to hit up https://annualcreditreport.com and hit “Request yours now!” on that top bar. Once you do that, you’ll be presented with:

You’ll be presented with a form that you’ll need to fill in with your personal information including name, social, address, etc. If you have not been at your current address more than 2 years, you’ll also need to provide any previous addresses within that time frame. After doing all that, you’ll reach:

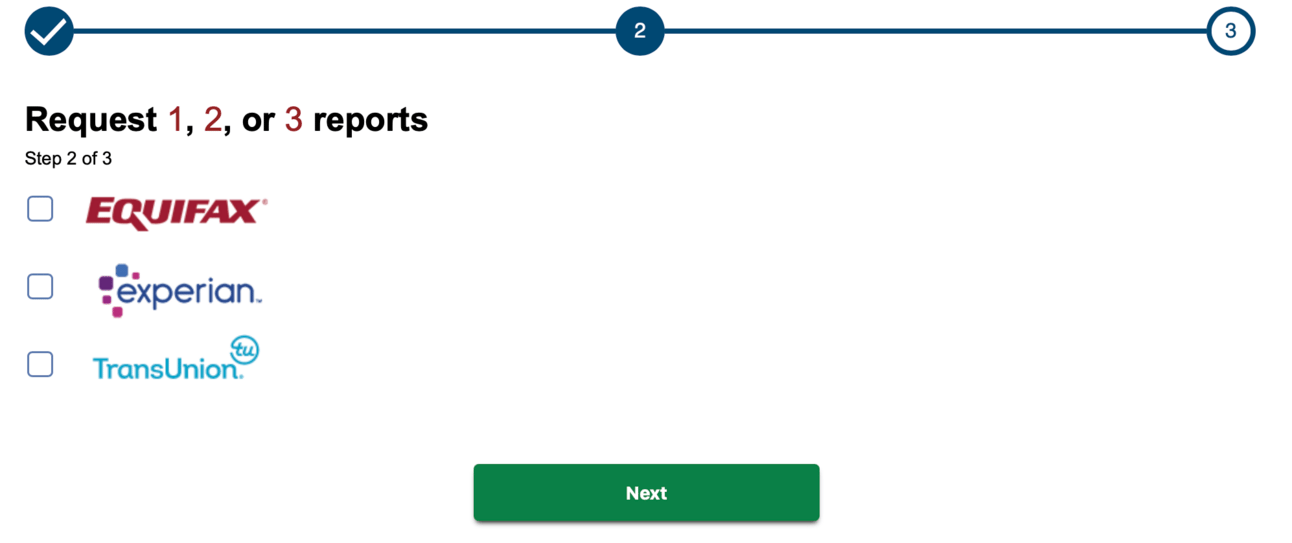

Here’s where you have a choice, you can run all three at the same time, or just select one you want to go through. Should you run all three? Should you just do one? Well, that’s completely up to you and what your goals are. They give some good advice below that:

If you are thinking about buying something big soon - a new car or even a home - you may want to get all of your credit reports now. That way you can correct any mistakes on all of them right away. If you are not planning a big purchase, requesting them over time might be a better choice. When you spread them out, watch for expected changes or suspicious activity throughout the year. Whichever strategy you choose, mark your calendar so you know when you can request your next free credit report.

Can’t put it much better than that. Again, doing all of them or only one of them at a time will not affect your credit score in any way. Do what works for you.

Each report will ask you to verify your identity via phone number and email address. If you’ve already got an account with the bureau(s) you’re running it on, use that email. If not, it’s kind of a crapshoot - but try the email you use the most (or know you have lines of credit registered to). I had to try a couple times with Transunion to find the right one.

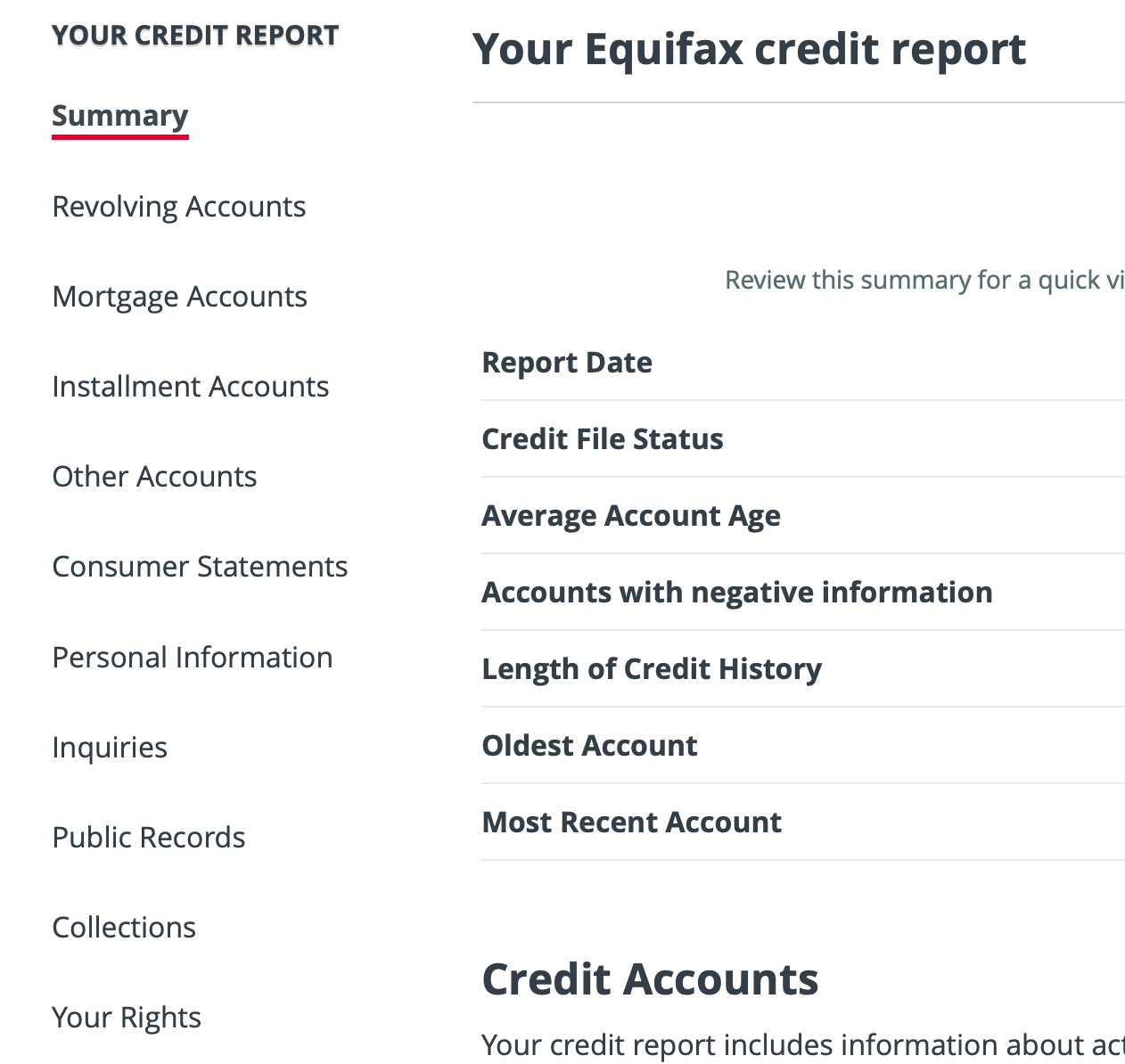

After verification, that’s it - you’ll have your credit report available to view and/or print off (or just save to pdf). Here’s some of the stuff included from my Equifax report:

A lot of good stuff in here, such as:

- All lines of credit you have open currently

- History of each credit line you’ve ever had, including if you made payments on time, current balance, limits, payment history, date opened/closed, etc.

This is where you’d look through to make sure everything lines up with what you know about your credit history. See a line of credit you never opened? An old school loan you completely forgot about that’s gone delinquent? Time to start making phone calls!

Wrap up

That about covers it, consider it your yearly checkup to make sure everything’s going as expected. And again, it’s free and doesn’t affect your credit score by doing it - so I highly recommend setting yourself a reminder and going through the trouble of getting it done yearly.

Jake